After Lunar New Year, the market has crashed and has been recovering. On 6 Mar 2024 (Wed), all indicators suggested by the strategy suggest to move onto risk assets.

The model allocated the first stock 601600 (大秦铁路). Interesting, this is the value stock that I’ve been tracking, who pays consistent dividend over the past years. Nowadays, one norm of the market is on the value investing, where the fundamental logic might not be the risk on, but instead, the rate cut that’s happening right now.

The fact that the bond market is running bull is due to the rate cut. With the discounting rate decreasing, the bond is benefiting directly and price is constantly moving up. The 5y and 10y treasury bonds that I’ve tracked in CTA model have moved up considerable.

The value stocks who pay dividends consistently benefited from rate cut as well. Such stocks include SOE banks, coal mining groups, railway companies, and etc. From last Nov till this Mar, both banking and mining stocks have increased considerable in market prices.

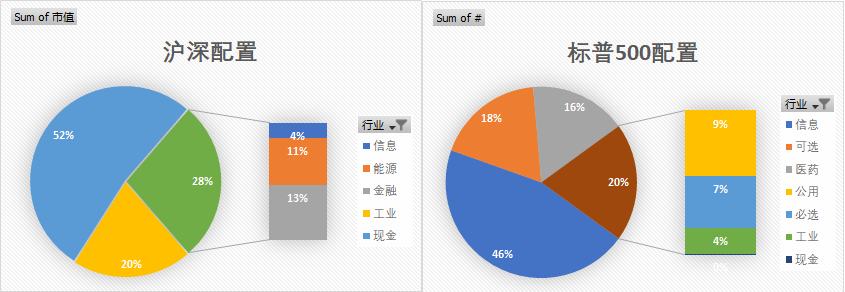

US market is fully allocated; the model is lagging behind the index, but it’s trending up. I would expect that US stock market would have turbulence when the election starts, but I will let the model to work it out, and I just need to track it closely.